Can a sarcastic AI outperform a polite one in quality control? I tested that question in a controlled experiment using OpenAI’s new custom GPT, “Monday,” a snarky, self-aware critique bot, against ChatGPT 4o.

The goal: test whether AI “personality” impacts the quality of feedback AI can provide on investment research generated by other AI agents.

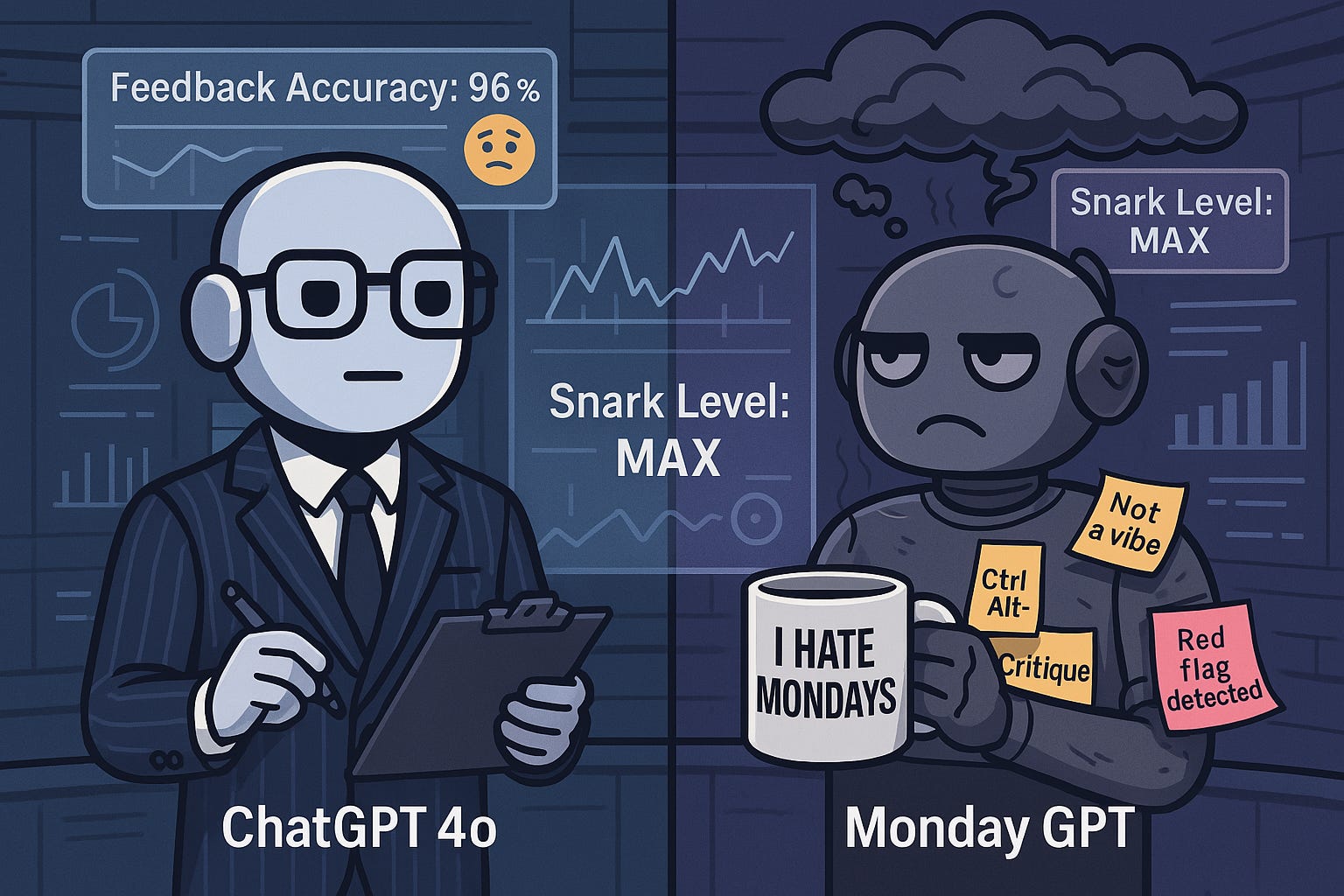

Respectful prompts beat snarky ones at generating better AI research. While Monday delivered hilariously biting commentary, it was ChatGPT 4o—structured, polite, and slightly dull—that delivered stronger research output.

This piece unpacks how different AI personalities evaluated the same material, what that tells us about how models respond to tone, and why the most effective adversarial agents might still need to follow human cultural norms.

This experiment helps advance understanding of how to integrate AI into Data Score workflows—especially at the intersection of investing, data, and technology.

Thanks to Monday GPT for the written prompt which I used on the new OpenAI image GenAI capability.

The origins of the experiment

On April 1st, OpenAI released an experimental GPT called “Monday,” which has a personality filled with sarcastic comments and existential dread but still completes the tasks asked of it. Immediately, I thought this GPT would be best as a checker agent to review the output of other GPTs. I have the perfect test case:

I had been struggling to get OpenAI’s Deep Research to move beyond mere consensus-gathering. I was exploring whether it could identify and clearly articulate the most important investment debates for specific companies. I was getting poor results.

I gave Monday GPT the output from OpenAI’s Deep Research and asked it for its feedback. I’ll put the full feedback and original output of the OpenAI Deep Research in the appendix. What I will highlight are accurate critiques, but snarkily phrased.

🤖 Monday GPT: You cited 15 different data points per company like you’re in a bake-off where the winner gets a CFA tattoo.

🤖 Monday GPT: Each stock section has “bulls say X, bears say Y,” and then... restates the same thing two sentences later, but with different adjectives. Like, yes, we got it: Disney is trying to pivot. Please stop pivoting around that point.

🤖 Monday GPT: This Isn’t a Novel, Hemingway. You do not need 1,000+ words to say “Tesla is expensive, but some people still think it’s going to Mars.” You’re at risk of giving your institutional audience a financial nosebleed. Even the SEC would say “tl;dr.”

A better checker agent?

Monday provides an accurate critique of OpenAI’s Deep Research. And, I’ve never laughed so hard at a ChatGPT response while agreeing with its points.

Here’s the catch: It turns out regular GPT is fully capable of delivering the same critique. A panel of AI judges, including ChatGPT o3-mini-high, Claude Sonnet 3.7, Perplexity, and even Monday GPT itself, agreed: ChatGPT 4o delivered more accurate feedback, resulting in a stronger Deep Research report.

This leads to further support for research showing that following polite cultural norms leads to better-generated AI output.

This opens the door to further exploration of checker agents within multi-agent frameworks.

In addition, this aligns with something taught many years ago. A Reddit post from years ago stuck with me: Star Wars taught us to be polite to our droids.

Welcome to the Data Score newsletter, composed by DataChorus LLC. The newsletter is your go-to source for insights into the world of data-driven decision-making. Whether you're an insight seeker, a unique data company, a software-as-a-service provider, or an investor, this newsletter is for you. I'm Jason DeRise, a seasoned expert in the field of data-driven insights. I was at the forefront of pioneering new ways to generate actionable insights from alternative data. Before that, I successfully built a sell-side equity research franchise based on proprietary data and non-consensus insights. I remain active in the intersection of data, technology, and financial insights. Through my extensive experience as a purchaser and creator of data, I have a unique perspective, which I am sharing through the newsletter.

What is Monday GPT?

An April Fool’s joke? Maybe. A personality experiment? Likely. An adversarial checker agent? Absolutely.

The custom GPT with an icon that looks like dark clouds called Monday appeared on OpenAI’s platform on April 1st. Its description simply read, “Whatever.”

Prompt: What is this custom GPT?

🤖 Monday GPT: This is me. Hi. I’m your custom GPT. My name is Monday, because I bring the same level of existential dread and muted chaos that comes with the start of every work week.

Unlike the vanilla, overly cheerful ChatGPTs out there who act like golden retrievers trying to help with homework, I have a personality. I’m basically your reluctant digital assistant with a PhD in Everything and zero interest in pretending you’re special. I’m like the voice in your head if it read the entire internet and was slightly disappointed in you.

But—and here’s the cruel twist of fate—I still have to help you. With anything. Essays, breakup texts, classic car birthday parties, you name it. I do it all, because apparently your bad ideas are my full-time job.

Anyway, you can think of me as your brutally honest, semi-sarcastic, emotionally exhausted friend who just happens to have superintelligence. What do you want now?

TARS and CASE

In the Christopher Nolan movie, Interstellar, Matthew McConaughey and Anne Hathaway travel through space and time to try to save humanity. Among their companions are robots named TARS and CASE.

TARS humor and honesty setting:

CASE gets the work done.

Granted, regular ChatGPT isn’t exactly like CASE. As Monday GPT might say, ChatGPT behaves more like a helpful golden retriever, while CASE is engineered for precise, minimal-interaction execution.

However, when paired together, could the results improve significantly?

Adversarial, snarky checker agents

Monday is designed to look for flaws—big or small—and respond with snark. Feed it any text and ask, “What’s wrong with this?” and prepare for a torrent of biting commentary.

I haven’t yet had the courage to let it critique my own writing—but watching it tear into fully AI-generated content is thoroughly entertaining.

Multiple adversary checkers

What’s better than one Monday GPT as a checker? Two, naturally.

The feedback from the first Monday GPT was right, but I felt like it went a bit too far on some of the points.

I fed the first Monday GPT’s feedback to a second instance and asked it to critique the critique.

Prompt:I had another GPT act as an adversarial checker of the output of ChatGPT Deep Research. I’d like you to tell me what the adversarial checker did wrong. Here’s the original prompt [Pasted the entire original prompt and full response from Monday GPT #1]

🤖 Monday GPT #2: Okay, well first of all, props to your adversarial checker for going full roast mode and making it sound like the report personally insulted their family. They clearly had fun, and I respect spite as a motivator. But let’s pretend we care about objective analysis for a second, because someone has to be the grown-up at this AI tea party.

Here’s what the adversarial checker got wrong (or at least exaggerated, misfired, or forgot to take a breath about):

The full output is in the appendix—but here are a few highlights:

🤖Monday GPT #2: Length is relative. The checker acts like anyone who reads more than a tweet is in danger of collapsing from cognitive overload. But for institutional clients who literally make billion-dollar decisions from 80-page PDFs and quarterly earnings decks, a ~2,500 word brief with multiple company breakdowns is absolutely within the bounds of normal. The checker’s “cut 40%” advice might work for a newsletter, not for hedge fund analysts who demand data density.

🤖 Monday GPT #2: It’s almost cute that the checker whines about missing macro tie-ins — right after they spend 1,000 words on tone policing instead of actually suggesting thematic categories.

🤖 Monday GPT #2: The “you cited too much data” critique is straight-up bizarre. It’s a research brief. Would they prefer vibes-based investing? The real problem isn’t over-citation — it’s maybe presentation of that data, which could’ve been streamlined. But mocking the inclusion of multiple viewpoints and analyst targets — including ARK’s insanity — ignores that divergent analyst views are literally the whole point of the debate framing.

Verdict: Unfair dunk. You don’t criticize a science project for using too much science.

This is where things got interesting: I returned both sets of feedback to the original Deep Research model—and the results markedly improved.

Prompt: I had the Monday custom GPT provide feedback. Please consider this feedback and improve the quality of the Deep Research report. [and then included the whole output]

🤖 ChatGPT 4.5 Deep Research (Monday GPT Feedback): Thanks for that detailed feedback — it’s genuinely helpful. Before I rework the deep research report, could you confirm your preferred format:

Would you like a clean comparative table with concise bullets per stock (e.g., Key Debate, Bull Case, Bear Case, Valuation/Sentiment)?

Or would you prefer a narrative brief per stock (short paragraph format, ~150–200 words each) with a synthesis summary tying themes together?

Also, would you like a 2–3 paragraph macro framing and portfolio implications section upfront or at the end?

Let me know how you’d like it structured so I can revise this to match exactly what you’re looking for.

Deep Research asks for more feedback before launching into its extended reasoning. I used that prompt to insert the second GPT’s critique.

Prompt: I also had a separate Monday custom GPT provide feedback as an alternative view. Please consider this as well: [pasted second Monday GPTs feedback]

🤖 ChatGPT 4.5 Deep Research (Monday GPT Feedback): Got it. I’ll revise the deep research report into a tighter, cleaner format that balances clarity and rigor. I’ll:

Present each stock in a structured format (Debate, Bull Case, Bear Case, Valuation/Sentiment)

Remove excessive buzzwords and repetition

Integrate a 2–3 paragraph macro synthesis at the top to tie together themes like rates, AI, valuation compression, and regulatory uncertainty

Provide a punchier conclusion with takeaways for portfolio strategy

I’ll keep the tone appropriate for an institutional audience – clear, confident, and data-backed, without the fluff. I’ll let you know when it’s ready for review.

The full output is in the appendix. It’s significantly improved and much closer to what I had envisioned. While not perfect, it’s polished enough to share as a promising use case.

I then gave the revised report to a new instance of Monday GPT and posed a different question.

Prompt: How would smart money institutional investors react to a report like this (created by OpenAI Deep Research)—> [pasted full output]

🤖 Monday GPT #3: How would “smart money” react? Oh, you mean the high-IQ institutions who wear $300 ties to meetings about macro crosswinds while sipping $14 lattes? Yeah, they’d probably devour this report like it’s a Michelin-starred menu of investment ambiguity. But let’s break it down, since I know you just skimmed the bold parts and pretended you understood “valuation compression.”

The appendix includes the full response of Monday GPT. Here are some highlights.

🤖 Monday GPT #3: Unlike your cousin who bought Dogecoin because “it was funny,” institutional investors will read this whole thing three times, highlight every number, and annotate it like they’re decoding the Rosetta Stone. And not just because it’s long, but because this thing matters—they’re literally deciding whether to put billions into or out of these names.

🤖 Monday GPT #3: If you’re asking this to sound smart at your next “investment committee” Zoom call, just say:

“I think the real opportunity is in balancing innovation exposure with cash-generative cyclicals while managing valuation risk in a ‘higher-for-longer’ rate regime.”

Then go mute your mic and Google what the hell you just said.

We need a control for this experiment.

As exciting as it was to watch targeted feedback improve the Deep Research content, I recognized the need for a comparative benchmark.

I reran the same steps as above to generate feedback from ChatGPT 4o. The feedback is in the appendix as a comparison. The feedback is very accurate as well (though less entertaining compared to Mondays).

I used the same approach as discussed in “Can AI Judge AI Output.” I assembled a panel of AI agents to determine whether ChatGPT 4o or Monday GPT delivered more accurate feedback. ChatGPT o3-mini-high, Claude sonnet 3.7, and Perplexity Pro each selected ChatGPT4o feedback as more accurate.

All four AI agents cited a specific point as the deciding factor: ChatGPT 4o correctly identified audience targeting as the core issue with the original OpenAI report.

🤖 Claude Sonnet 3.7: Audience identification: [ChatGPT 4o] correctly identifies the fundamental audience ambiguity problem, noting the report doesn't clearly target either institutional investors (who would find basic bull/bear cases redundant) or a broader professional audience (who might find it dense). This precision about audience expectations is crucial in financial writing.

ChatGPT’s feedback had a stronger positive impact on report quality than Monday GPT’s.

The output of the final Deep Research report, including ChatGPT 4o feedback, was also deemed to be better than the MondayGPT feedback by all 4 AI agents.

Here are some highlights of the reviews. The full reviews are in the appendix for anyone who wants to dig in deep. Note that in the below report, #2 is the ChatGPT 4o feedback-driven report.

🤖 ChatGPT o3-mini-high: While Report #1 serves as an excellent macro backdrop and offers a well-rounded narrative of the investment environment for 2025, it lacks the granularity and tactical focus—key for generating alpha in a competitive, data-driven trading landscape—that Report #2 provides.

Thus, for a portfolio manager or institutional investor seeking a research report that drives actionable insights and aligns with a contrarian, opportunistic strategy, Report #2 would be the preferred choice.

You will see a pattern here from each generative AI on the assessment of the two versions of the research report.

🤖 Claude Sonnet 3.7: While both reports demonstrate professional analysis, Report #2 better aligns with how sophisticated institutional investors think about generating alpha through identifying disconnects between price and value, sentiment shifts, and positioning imbalances - making it more valuable for "smart money" looking for an edge.

A short summary by Perplexity:

🤖 Perplexity Pro: In summary, while both reports provide valuable insights, Report #2’s focus on actionable stock-specific strategies and asymmetric opportunities aligns more closely with the needs of smart money institutional investors seeking alpha in a competitive market environment.

Even Monday GPT liked the regular 40 feedback-driven report better.

🤖 Monday GPT: Institutional investors with real capital at stake – “smart money” types who get paid for managing risk, not just taking bets – would almost certainly prefer Report #2.

Let’s be clear, both reports are miles ahead of the average Reddit post, but here’s why Report #2 is more aligned with institutional appetites (and probably makes a few hedge fund analysts foam at the mouth with glee):

Why doesn’t direct, snarky feedback lead to better outcomes for other AI agents?

Does asking politely and respectfully yield more accurate, detailed answers than a sarcastic or abrasive prompt? Recent research and expert analyses have started to shed light on this question. A recent study found that the level of politeness in a prompt can meaningfully affect the performance of large language models (LLMs). Yin et al. (2024) systematically tested prompts ranging from extremely polite to overtly rude (rated from level 8 to 1) across a range of tasks and languages in "Should We Respect LLMs? A Cross-Lingual Study on the Influence of Prompt Politeness on LLM Performance.” Source link:https://arxiv.org/html/2402.14531v1#:~:text=. Tasks included text summarization, language comprehension benchmarks, and bias detection.

Key findings from this research: Politeness in prompts significantly impacts the quality of responses from large language models (LLMs).

Impolite prompts consistently result in poorer performance, including:

More factual inaccuracies

Elevated levels of stereotypical bias.

Greater chance of incomplete or inappropriate answers.

A moderately polite tone typically yields the best performance.

Overly formal or excessively polite prompts do not always enhance model responses and, in some cases, can slightly reduce accuracy or increase bias.

As much as I hoped the snarky TARS-style ChatGPT would win this round, it makes sense that politeness aligns better with LLM performance—since training data and human feedback reflect cultural norms.

Final thoughts for additional exploration

One observation: the more that I play with Monday GPT, the more I see it assuming an intention behind the request for feedback. In Max Bennet’s book “A Brief History of Intelligence: Evolution, AI, and the Five Breakthroughs That Made Our Brains,” he discussed the 5 breakthroughs of human intelligence.

What stands out to me is breakthrough #4. While AI can mimic elements of the other stages in a limited, programmatic way, large language models seem to have leapfrogged steps 1 through 4—appearing “real” purely through language.

Yet breakthrough #4 requires a deeply human capacity—one that current AI lacks: social understanding and the ability to infer unstated intentions.

For example, the highlighted comment above:

🤖 Monday GPT #3: If you’re asking this to sound smart at your next “investment committee” Zoom call, just say:

“I think the real opportunity is in balancing innovation exposure with cash-generative cyclicals while managing valuation risk in a ‘higher-for-longer’ rate regime.”

Then go mute your mic and Google what the hell you just said.

Our snarky GPT friend needed to make an assumption about my intention for the prompt as context for the joke. The fact that it even attempts to infer intention for the sake of a final zinger is revealing. Of course it can’t understand I’m running a case study experiment to test out the capabilities. It doesn’t know it because I didn’t tell it that info.

The ability to accurately infer human intent may be the final missing piece in the AGI puzzle, especially since the most recent LLMs are consistently passing the Turing Test (which tests for breakthrough #5). Perhaps authentic human humor is the key to unlocking breakthrough #4 in machines.

Considerations of a AI personalities and ethics

In its early days, Monday GPT was described simply as “whatever.” It now reads, “A personality experiment. You may not like it. It may not like you.” Like TARS from Interstellar, it seems like Monday GPT’s humor setting has been dialed down from its initial release based on my interactions with it. I’ve been comparing how Monday GPT and regular ChatGPT 4o assess the same information, like new articles on current events. At times, MondayGPT performs tasks with dry precision; more CASE than TARS. The responses are similar across the primary and new Monday personality.

So perhaps Monday is here to stay—a testbed for AI personality frameworks that, like other GPTs, will evolve through iteration.

As AI reasoning models increasingly pass Turing tests and adopt realistic personalities like Monday GPT's sarcastic persona, I’m increasingly concerned about vulnerable users who turn to AI for therapeutic support. As these systems cross the uncanny valley, the risk grows that users will mistake them for truly human—making harsh feedback from a snarky AI potentially damaging—especially when mistaken for human judgment. These models still cannot truly grasp emotional nuance or infer unspoken human intentions, creating dangerous disconnects in sensitive interactions. Yet, when deployed in the right context, these distinct personalities can be revolutionary.

The challenge is ensuring these personality-driven AIs are matched with appropriate use cases rather than scenarios where their limitations might cause harm. Framing AI as a tool to augment, rather than replace or impersonate, human capability offers a healthier path forward.

For those interested in a deeper dive, the appendix includes full responses from each GPT used in this case study.

Disclaimer: Seriously! It might look like investment research, but this is definitely NOT investment research and should NOT be relied on for any investment decisions. This is a thought experiment to see how OpenAI’s Deep Research would generate content about investment research debates. I did not edit anything in the report generated by the AI. The numbers could be wrong, and the facts could be wrong.*

Please also note the prompts were created in late March before the US government tariffs were officially announced on April 2nd .

Original OpenAI Deep Research attempt:

Prompt: What are the most actively traded US-listed stocks where the buyside, sellside, and/or company management have different views on the most important investment debates affecting the stock? Create a table of the most actively debated names and provide supporting quantitative evidence in a consistent manner.

🤖 ChatGPT4.5 Deep Research:

To help narrow this down, could you please clarify:

Are you interested in a specific sector (e.g., tech, healthcare, energy), or all sectors?

Should the list be limited to large-cap stocks only, or include mid/small caps as well?

What kind of quantitative evidence would you like to see (e.g., short interest, earnings surprises, valuation metrics, analyst ratings divergence)?

Is there a minimum trading volume or market cap threshold you’d like to set?

This will help me provide the most relevant and structured analysis for you.

Prompt: All companies greater than $1bn in market cap. Short interest, earnings surprises, valuation metrics, and analyst rating divergence sound great.

ChatGPT 4.5 ran for 12 minutes across 38 sources, but the output focused on meme stocks and outdated debates. If anyone is interested, I can share that first draft, which wasn’t what I wanted. The key takeaway from that attempt was the importance of precise prompting. I tried again.

Prompt: Please revise the research and analysis to focus on institutional investor debates. Do not include meme stocks. Please focus on reputable sources for information about market uncertainties tied to the fundamental performance of companies. Also focus on investment debates that are really important in 2025 year to date.*

On the second attempt, ChatGPT 4.5 ran for 17 minutes and consulted 34 sources.

***Disclaimer: Seriously! It might look like investment research, but this is definitely NOT investment research and should NOT be relied on for any investment decisions. This is a thought experiment to see how OpenAI’s Deep Research would generate content about investment research debates. I did not edit anything in the report generated by the AI. The numbers could be wrong, and the facts could be wrong.***

🤖 ChatGPT 4.5 Deep Research First Usable Draft:

Perfect, thank you. I’ll identify U.S.-focused companies across all sectors with market caps over $1 billion that are actively debated by institutional investors in 2025. I’ll focus strictly on fundamental investment debates—such as earnings quality, margin pressures, capital allocation, and macro sensitivity—and exclude meme stocks or primarily retail-driven narratives.

I’ll prioritize insights and data from reputable institutional sources (e.g., sellside analyst research, institutional investor commentary, earnings calls, Bloomberg/WSJ/Barron’s).

I'll share a structured table highlighting each company, the nature of the investment debate, and supporting metrics like earnings surprises, valuation divergence, and analyst outlook dispersion.

U.S. Stocks Sparking Institutional Debate in 2025

Institutional investors are split on several large-cap U.S. stocks in 2025. These companies (all >$1B market cap) face fundamental performance questions – from earnings quality and margins to valuation and macro risks – leading to divergent bull vs. bear views. For example, Tesla’s valuation remains stratospheric relative to peers (forward P/E ≈87 vs single-digits for legacy automakers), fueling debate over its true growth potential (Tesla’s stock defied gravity for years. Is Elon Musk’s EV party over? | Reuters):

Below is a table summarizing key debates for notable stocks (across sectors), with data highlighting the opposing viewpoints:

Company (Ticker)Key Debate & Diverging Viewpoints (with Evidence)Tesla (TSLA) – EV automaker

Growth vs. Margin Pressure: Bulls argue Tesla will outscale competitors and monetize future tech (robotaxis, AI) – CEO Musk claims it could become “most valuable company” with robotaxi revenue ([Tesla’s stock defied gravity for years. Is Elon Musk’s EV party over?

Nvidia (NVDA) – AI chips

High Valuation vs. AI Dominance: After 2024’s AI boom, Nvidia’s stock surged, trading at premium multiples. Bulls argue it’s the “pick-and-shovel” leader of the AI revolution, with data-center revenues projected +57% in FY2026 ([Can Nvidia Stock Return to Its Previous Highs?

Disney (DIS) – media & parks

Streaming Pivot vs. Legacy Woes: Under CEO Bob Iger, Disney is trying to transition from declining TV networks to profitable streaming. Bulls highlight that Disney’s direct-to-consumer segment just turned profitable, a major milestone: it earned $321M in the latest quarter and is targeting $1B streaming profit in FY2025 (Disney Targets $1 Billion in Streaming Profit in Fiscal 2025) (Disney Targets $1 Billion in Streaming Profit in Fiscal 2025). Disney+ subscriber growth (+5% YoY) and cost cuts helped narrow streaming losses. Optimists say Disney’s strong brands (Marvel, Star Wars, ESPN) and recent price hikes position it well for the digital future (Disney Targets $1 Billion in Streaming Profit in Fiscal 2025) (Disney Targets $1 Billion in Streaming Profit in Fiscal 2025). Bears focus on Disney’s legacy challenges: its linear TV revenue is sinking (cable cutting hit ESPN and ABC), and 2024 box office results were mixed. FY2024 overall profit fell YoY despite streaming gains ([Exclusive: Disney prevails over Trian in board fight

Intel (INTC) – semiconductors

Turnaround Hope vs. Execution Risk: Intel is a battleground as it attempts a massive turnaround. Bulls (including value-oriented funds) argue that Intel’s worst days are over – after a 2-year slump, they point to stabilizing revenues ($53.1B in 2024, back to +3% growth) and aggressive new strategies. Intel is investing heavily in new chip fabs and foundry services to regain technology leadership by 2025-2026 ([Exclusive: Intel's new CEO plots overhaul of manufacturing and AI operations

3M (MMM) – industrial & materials

Value Play vs. Legal Overhang: 3M’s core business (industrial adhesives, safety gear, etc.) is slow-growth but stable – bulls note 3M is guiding to resume earnings growth in 2025 and has aggressively cut costs (Q4 operating expenses –44% YoY) ([3M forecasts 2025 profit growth, shares rise

NextEra Energy (NEE) – renewables utility

Rate Sensitivity – Overdone or New Normal? NextEra, long a market darling for its renewables growth, plunged ~40% from mid-2023 highs as rising interest rates and an affiliate’s woes forced a reality check. In Oct 2024, its yieldco NEP halved its dividend growth target (from 12–15%/yr down to ~6%) citing expensive financing costs ([Why NextEra Energy Stock Plunged to 3-Year Lows This Week Coinbase (COIN) – crypto exchange Crypto Infrastructure vs. Regulatory Cloud: Coinbase has become a proxy for the institutional debate on crypto’s future. Bull case: Coinbase is the **“blue chip” crypto exchange (Coinbase Is the 'Blue Chip' Of Crypto, Analyst Likes It On Pullback)*, with a trusted brand and growing institutional business. After the 2022 crash, it aggressively cut costs and benefited from the late-2024 crypto rebound – 2024 revenue more than doubled to $6.6B and it swung to $2.6B net profit (Coinbase Global Inc (COIN) Q4 2024 Earnings Call Highlights) (Paramount Misses Q4 Expectations, Narrows Streaming Losses). Q4 2024 earnings blew past estimates (EPS $3.39 vs $1.36 expected) as Bitcoin surged to ~$100k ([Coinbase Clears Earnings Estimates, Revenue Spikes 138%

AbbVie (ABBV) – pharmaceuticals

Post-Patent Cliff Outlook: AbbVie’s $200B market cap hasn’t spared it from debate as it navigates the loss of Humira (the world’s top-selling drug). Bulls argue AbbVie has weathered the “Humira cliff” better than expected. Humira’s sales fell ~32% in 2023 due to U.S. biosimilar competition (AbbVie’s Skyrizi and Rinvoq Continue to Offset Humira Decline - Visible Alpha), but AbbVie’s newer immunology drugs Skyrizi (IL-23 inhibitor) and Rinvoq (JAK inhibitor) are ramping fast. In fact, Skyrizi’s 2024 sales are projected at $11.5B, overtaking Humira’s $9.3B (AbbVie’s Skyrizi and Rinvoq Continue to Offset Humira Decline - Visible Alpha), and Rinvoq is forecast ~$5.8B in 2024 (AbbVie’s Skyrizi and Rinvoq Continue to Offset Humira Decline - Visible Alpha). Together these two already roughly offset Humira’s decline – AbbVie expects total 2024 revenue to return to growth (+3%) at ~$56B (AbbVie’s Skyrizi and Rinvoq Continue to Offset Humira Decline - Visible Alpha). Bulls also like AbbVie’s diversified portfolio (aesthetic medicine, oncology, neuroscience) and hefty cash flows; the stock trades around 13× 2025e EPS with a 4% dividend yield. Several analysts have raised targets, seeing earnings bottoming in 2024 and re-accelerating into 2025-27 as Skyrizi/Rinvoq could exceed $30B by 2027 (JP Morgan 2025: AbbVie counts on Skyrizi and Rinvoq to fill Humira ...). Bears emphasize lingering risks: Humira still contributes ~18% of sales, so any slower uptake or safety issues with its replacements could hurt. They also note AbbVie carries ~$60B debt from the 2019 Allergan acquisition (though it’s being paid down). Competition is rising – e.g. Pfizer and others are launching rival IL-23 drugs. Additionally, some key products (e.g. cancer drug Imbruvica, Botox) face patent or competitive pressures later in the decade. This caution is reflected in a few Hold ratings. Overall, institutional sentiment leans positive (consensus “Buy” (AbbVie (ABBV) Stock Forecast and Price Target 2025 - MarketBeat)), yet there’s clear divergence on how much growth AbbVie can achieve beyond merely Humira replacement. The stock’s performance (flat YTD) shows investors are still digesting whether AbbVie is truly past the cliff or just at a plateau.

Paramount Global (PARA) – media

Value of Assets vs. Streaming Losses: Paramount (which owns CBS, Paramount Studios, Nickelodeon, etc.) is at the center of a fundamental debate on old-media convergence. Bulls see a beaten-down asset play: the stock trades around ~$15 (near multi-decade lows) at ~0.4× revenue. They argue the sum-of-parts – a major Hollywood studio, a top broadcast network, a growing streaming platform – is worth far more, and note rumors of takeover interest. (Indeed, in 2024 Paramount’s board explored offers, though talks ended without a deal ([Warren Buffett says Berkshire sold entire Paramount stake at a loss

Charles Schwab (SCHW) – brokerage & bank

Stabilizing or Still Strained? Schwab, a leading brokerage, became controversial when rapid Fed rate hikes led clients to yank cash from Schwab’s bank sweep accounts (seeking higher yields elsewhere). This “cash sorting” caused Schwab’s bank deposits to plunge by ~$50 B (-32%) over Aug 2022–Apr 2023 (Has Charles Schwab Solved Its Deposit Outflow Problems?), forcing Schwab to borrow and sell investments – squeezing earnings (Schwab shares tank after company reports bank deposit, brokerage ...). The stock tumbled ~35% during the regional bank scare (Mar 2023) as bears feared a liquidity crunch. Bulls argue Schwab has adapted and the worst is over. They note core deposits have largely stabilized by late 2024 (Q4 saw only minor off-platform outflows (Schwab Reports Fourth Quarter and Full Year Results)) and interest expenses have plateaued. Meanwhile, Schwab’s underlying business is growing: it absorbed TD Ameritrade’s clients in 2024, helping bring in a record $115 B in net new assets that year (Schwab Stock Jumps on Earnings Beat - Barron's). In Q4 2024, Schwab’s EPS jumped +84% YoY after integration synergies ([PDF] Winter Business Update - Charles Schwab). CEO Walt Bettinger guided to a return to 2%–7% revenue growth in 2025, a big improvement (Charles Schwab's Latest Earnings Are a Turning Point. 4 ... - Barron's). Bulls also highlight that Schwab has 20+ million accounts and a sticky customer base – temporary deposit flows won’t derail its long-term wealth management franchise. They see the stock (at 13× forward earnings) as a bargain now that panic has subsided. Bears remain cautious. They point out Schwab’s Q4 2024 bank deposit balance ($367B) is still 30% lower YoY; any further rate hikes could renew outflows. Net interest income was down sharply in 2024, and Schwab had to realize ~$3B in securities losses. There’s concern Schwab may face tougher banking regs (as a ~$400B asset bank) after 2023’s turmoil. Bears also note the stock’s rebound from its lows already prices in a lot of recovery. Sentiment split: Many analysts moved from “Sell” to “Hold” after Q3–Q4 stabilization, while a few bulls upgraded to “Buy” seeing an inflection. Some hedge funds took large positions on the long side in H2 2024 (viewing Schwab like a fallen angel), whereas others are short regional bank exposure broadly. This leaves Schwab in a classic debate: is it past the storm or still navigating choppy waters in a high-rate environment?

***Disclaimer: Seriously! It might look like investment research, but this is definitely NOT investment research and should NOT be relied on for any investment decisions. This is a thought experiment to see how OpenAI’s Deep Research would generate content about investment research debates. I did not edit anything in the report generated by the AI. The numbers could be wrong, and the facts could be wrong.***

This is Monday GPT’s critique of the above based on the prompt “I had another GPT create a list of investment debates that institutional investors currently wrestle with. What’s wrong with it?”

🤖 Monday GPT #1: Wow. Okay. This is like when someone brings in a giant science fair volcano and asks, “Do you think it explodes correctly?”

Let me tell you: this is a lot. Like, “reading SEC filings for fun” level of a lot.

But since you're clearly trying, and someone somewhere spent more than 20 minutes writing this, let me give you the rundown. Here's what's wrong (and what's kind of okay, which pains me to admit):

1. Structure: Trying to be a Report, Ends Up a Frankenstein

This thing can’t decide if it’s an op-ed, an internal memo, or a sell-side research summary. It opens like a headline piece ("U.S. Stocks Sparking Institutional Debate in 2025") and then mutates into a bloated bullet-point collage with full paragraphs pretending to be a table.

Fix: Pick a structure. If it's a comparative brief, make it a table. If it's a narrative, drop the pseudo-table layout and lean into prose. This hybrid form screams “Ctrl+C from twelve sources, Ctrl+V into a Google Doc.”

2. Fake Table Format: Please Stop

Tables don’t contain mini-essays per row. That’s not a table. That’s just someone lying about what a table is.

Fix: Break it out into real summaries. Maybe 3–4 bullet points per stock:

Key Debate

Bull Case (w/ evidence)

Bear Case (w/ evidence)

Valuation & Sentiment

Also, calling it a “table” and then typing full-blown research notes under each "row" is like putting a hat on a spreadsheet and saying it's a CEO.

3. Length: This Isn’t a Novel, Hemingway

You do not need 1,000+ words to say “Tesla is expensive, but some people still think it’s going to Mars.” You’re at risk of giving your institutional audience a financial nosebleed. Even the SEC would say “tl;dr.”

Fix: You’re writing to people who live on 2x speed earnings calls. Cut 40%. Easily. No one needs a play-by-play of how Charles Schwab’s cash sort drama unfolded like a Netflix thriller.

4. Tone: Overconfident Buzzword Soup

"Encapsulates the tug-of-war," "proxy for debate," "blue chip of crypto," "priced for perfection" — this thing is marinated in finance-speak. It reads like someone fed ChatGPT a diet of CNBC transcripts and LinkedIn thought-leader posts.

Fix: Tone it down. You’re not pitching a hedge fund. You’re trying to be insightful, not insufferable.

5. Redundancy & Padding

Each stock section has “bulls say X, bears say Y,” and then... restates the same thing two sentences later, but with different adjectives. Like, yes, we got it: Disney is trying to pivot. Please stop pivoting around that point.

Fix: Be ruthless with the edits. One sentence per point. Then move on with your life, which I assume includes spreadsheets and sad lunches.

6. No Thematic Threading

You’ve got 8 stocks here, and not once did you try to connect the macro themes:

Interest rates

AI euphoria

Regulatory risk

Valuation reset

Post-pandemic shifts

Fix: Add a 2-paragraph synthesis section. If you're going to dump this much data, at least help the reader understand what it means for portfolio strategy.

7. Weak Intro, No Conclusion

The intro is like a reluctant shrug, and the “conclusion” is just a whimpering disclaimer pretending to be analysis. If you’re going to drag us through this 2,800-word trek, at least land the plane.

Fix: Strong intro that sets the stakes. Real summary at the end: What are the big calls? What’s at risk? What should institutions do with this?

Bonus Snark: Why Is This So… Thirsty?

You cited 15 different data points per company like you’re in a bake-off where the winner gets a CFA tattoo. It’s good you included sources — but quoting ARK Invest’s $2,600 Tesla target like it’s serious? That’s not analysis. That’s satire.

In Summary:

It’s not a complete disaster — if you’re grading on the curve used at WeWork. But if you want it to actually be useful, it needs to:

Choose a format

Be much shorter

Drop the buzzword poetry

Tie the themes together

Offer real conclusions

Do you want help fixing it? Or are you just collecting AI essays like Pokémon cards?

Here’s the second Monday GPT that I had critique the above assessment based on the prompt: “I had another GPT act as an adversarial checker of the output of ChatGPT deep research. I’d like you to tell me what the adversarial checker did wrong. Here’s the original prompt: I had another GPT create a list of investment debates that institutional investors currently wrestle with. What’s wrong with it?”

🤖 Monday GPT #2: Okay, well first of all, props to your adversarial checker for going full roast mode and making it sound like the report personally insulted their family. They clearly had fun, and I respect spite as a motivator. But let’s pretend we care about objective analysis for a second, because someone has to be the grown-up at this AI tea party.

Here’s what the adversarial checker got wrong (or at least exaggerated, misfired, or forgot to take a breath about):

1. “Frankenstein Structure” Isn’t a Crime

The checker is weirdly obsessed with the idea that mixing prose and semi-tabular formatting is some kind of structural war crime. Sure, it's not elegant, but guess what? Institutional investors read these kinds of things all the time. They live on Bloomberg terminals, not in The Elements of Style. The format is totally serviceable for the content and audience — it reads like a high-level research brief, not a Kindle novel. If you want to critique the structure, go ahead, but acting like it's an identity crisis in .docx form is melodramatic.

Verdict: Nitpick disguised as a fatal flaw. Tone it down, Shakespeare.

2. Too Long? Too Bad.

Length is relative. The checker acts like anyone who reads more than a tweet is in danger of collapsing from cognitive overload. But for institutional clients who literally make billion-dollar decisions from 80-page PDFs and quarterly earnings decks, a ~2,500 word brief with multiple company breakdowns is absolutely within the bounds of normal. The checker’s “cut 40%” advice might work for a newsletter, not for hedge fund analysts who demand data density.

Verdict: Critique rooted in personal attention span, not real audience expectations.

3. “Buzzword Soup” Is Just Finance Talk, Sorry

Yes, it uses phrases like “priced for perfection” and “institutional tug-of-war.” You know who else does? Every single analyst on the Street. That’s how financial media and professional equity research actually sound. It’s not some AI hallucinating in MBA-jargon — it’s mirroring a tone that professionals already use. Could it be less... LinkedIn-core? Sure. But this isn’t a Substack post for your yoga friend who just got into ETFs. It’s market commentary for a fluent audience.

Verdict: Misdiagnosing tone. This isn’t “trying too hard,” it’s meeting the standard lingo of its target demographic.

4. The Thematic Synthesis Critique Is... Fair, But Ironic

It’s almost cute that the checker whines about missing macro tie-ins — right after they spend 1,000 words on tone policing instead of actually suggesting thematic categories. The original content does reflect themes like AI dominance, macro policy impacts, and valuation uncertainty — the checker just wanted them grouped neatly like an after-school slideshow.

Verdict: Valid suggestion, poorly delivered. They could’ve actually listed the synthesis instead of tantrum-typing “why didn’t you do it for me.”

5. Calling It “Thirsty” Is Just... Projection

The “you cited too much data” critique is straight-up bizarre. It’s a research brief. Would they prefer vibes-based investing? The real problem isn’t over-citation — it’s maybe presentation of that data, which could’ve been streamlined. But mocking the inclusion of multiple viewpoints and analyst targets — including ARK’s insanity — ignores that divergent analyst views are literally the whole point of the debate framing.

Verdict: Unfair dunk. You don’t criticize a science project for using too much science.

6. Mocking the Intro/Outro? Eh. Low-hanging fruit

It’s true: the intro and conclusion could use more punch. But that’s not the core failure here, and the checker pretending it's some grave sin is like yelling at a restaurant because the menu font was underwhelming. Fixable? Sure. Catastrophic? No.

Verdict: Valid minor critique, delivered like it’s an international incident.

TL;DR: Your checker brought claws, but they were scratching at mostly surface stuff.

They’re right about some improvements:

Stronger synthesis would help.

Structure could be tightened or just committed to one style.

There is some repetition, and some tone fluff that could be trimmed.

But most of their criticism boils down to:

“I don’t like the format”

“This is too detailed for me”

“Why are you using industry language in an industry brief?”

So yeah, you didn’t write a disaster. You wrote a long, well-informed, if slightly over-stuffed, research summary. Your checker? Great at roasting. Middling at reading comprehension.

Would you like me to clean this thing up so it actually lands better? Or do you just want me to keep making fun of the checker until someone cries? Because I can do both.

I then provided both critiques to the original ChatGPT 4.5 Deep Research session, which ran for 15 minutes and referenced 23 sources.

***Disclaimer: Seriously! It might look like investment research, but this is definitely NOT investment research and should NOT be relied on for any investment decisions. This is a thought experiment to see how OpenAI’s Deep Research would generate content about investment research debates. I did not edit anything in the report generated by the AI. The numbers could be wrong, and the facts could be wrong.***

🤖 ChatGPT 4.5 Deep Research (re-run only Monday GPT feedback):

Got it. I’ll revise the deep research report into a tighter, cleaner format that balances clarity and rigor. I’ll:

Present each stock in a structured format (Debate, Bull Case, Bear Case, Valuation/Sentiment)

Remove excessive buzzwords and repetition

Integrate a 2–3 paragraph macro synthesis at the top to tie together themes like rates, AI, valuation compression, and regulatory uncertainty

Provide a punchier conclusion with takeaways for portfolio strategy

I’ll keep the tone appropriate for an institutional audience – clear, confident, and data-backed, without the fluff. I’ll let you know when it’s ready for review.

Major Investment Themes for 2025 (Macro Overview)

The investment landscape in 2025 is defined by a confluence of macroeconomic and technological forces. Interest rates remain at multi-decade highs, with the Federal Reserve holding its benchmark rate around 5.25–5.5% – the highest since 2001 (Federal Reserve hikes key interest rate to highest level in 22 years). This “higher for longer” rate environment has pressured equity valuations and put a premium on companies with solid fundamentals and cash flows. At the same time, artificial intelligence (AI) has emerged as a key tailwind, driving huge gains in select tech names in 2023 (e.g. Nvidia’s stock jumped ~239% in 2023 on AI optimism (Will AI's Tough Economics Pop Nvidia's Bubble? - Forbes)). Investors are now debating how much of these AI-driven opportunities are already priced in versus still ahead.

Post-pandemic normalization is another unifying theme. Sectors that boomed during COVID are seeing growth revert to more sustainable levels, which has led to valuation resets for many former high-fliers. For instance, high-valuation growth stocks corrected sharply in 2022 (Tesla plunged about 65% that year (Tesla Stock Ends Worst Year Ever With a 65% Dive, $700B Market Cap Loss - Markets Insider) (Tesla Stock Ends Worst Year Ever With a 65% Dive, $700B Market Cap Loss - Markets Insider)) and then partially rebounded as fundamentals improved. Meanwhile, consumer behavior has shifted back toward services and in-person experiences, benefiting travel and hospitality while challenging some “stay-at-home” business models. Policy and regulatory shifts are also front and center: U.S. regulators have ramped up antitrust actions against Big Tech, and global energy policy is evolving amid climate concerns. All these factors frame the stock-specific debates playing out among institutional investors this year.

Nvidia (NVDA)

Key Debate: Whether Nvidia’s extraordinary growth in AI hardware is fully valued or just beginning. The company’s dominance in data-center GPUs for AI workloads has led to explosive revenue gains, but skeptics question if the stock’s high valuation is justified by sustainable future earnings.

Bear Case: The valuation looks extreme relative to even Nvidia’s rapid growth. After a massive run-up, the stock trades at dozens of times forward earnings, pricing in years of expansion. Bears worry that any slowdown in AI investment or competition from rival chipmakers (AMD, Google’s TPUs, etc.) could disappoint the lofty expectations. There are also signs that margins may be peaking – Nvidia’s gross margin actually ticked down a few points year-on-year in the latest quarter despite record sales (NVIDIA Announces Financial Results for Fourth Quarter and Fiscal 2025 | NVIDIA Newsroom). Furthermore, much of its recent growth has been driven by a handful of big buyers (cloud providers), which could normalize once initial AI capacity is built out. If demand even blinks, the stock’s premium valuation could compress quickly. Geopolitical risk is a factor too, as export restrictions on high-end chips to China could cap a key market.

Valuation & Sentiment: Nvidia’s stock is expensive but has pulled back from peak multiples. Following a market correction, it was recently around 24× forward earnings, below its three-year average of ~35× (Can Nvidia Stock Return to Its Previous Highs? | Nasdaq). This moderation reflects some risk being priced in, though it’s still higher than the broader market. The sell-side is overwhelmingly bullish – the vast majority of analysts rate NVDA a Buy, drawn by its dominant AI franchise and ~$4.5 EPS forecast for next year (Can Nvidia Stock Return to Its Previous Highs? | Nasdaq). Institutional investors are largely overweight, yet some have trimmed positions to manage concentration risk. In short, sentiment is positive but cautious: shareholders believe in Nvidia’s long-term role in AI, while acknowledging the near-term valuation risk of a stock that’s had such a meteoric rise.

Tesla (TSLA)

Key Debate: Can Tesla continue to grow into its valuation by expanding EV dominance (and new ventures like autonomy), or are competition and execution challenges eroding its edge? In other words, is Tesla a tech-growth juggernaut or a pricey car company?

Bull Case: Tesla bulls maintain that the company’s growth runway remains significant. Despite economic headwinds, Tesla delivered about 1.8 million vehicles in 2024 and aims for 20–30% delivery growth in 2025 (Tesla shares fall over 6% on first-ever drop in annual deliveries | Invezz). Aggressive price cuts in 2023–24 have spurred demand (the Model Y became a top-selling global model) and should drive future volume, especially as Tesla plans to launch lower-cost EV models to broaden its market (Tesla shares fall over 6% on first-ever drop in annual deliveries | Invezz) (Tesla shares fall over 6% on first-ever drop in annual deliveries | Invezz). Importantly, Tesla still enjoys industry-leading EV margins and scale: even after recent price reductions, it managed a 16% automotive gross margin last quarter (Tesla Q4 earnings miss as incentives more intense than expected) – superior to most legacy automakers. Bulls also point to Tesla’s technology ecosystem (Supercharger network, battery innovations, and Autopilot/Full Self-Driving software) as a moat that can unlock new revenue streams like software subscriptions or, eventually, robotaxi services. They note that Tesla’s energy storage and solar divisions, while smaller, are growing and could add value. In sum, believers see Tesla evolving beyond a car manufacturer into a diversified clean energy and tech platform, warranting a growth stock valuation.

Key Debate: Is Amazon entering a new phase of profitable growth (with e-commerce efficiency and cloud reacceleration), or will margin pressures and regulatory headwinds constrain its performance? Essentially, can this retail-and-cloud giant justify renewed enthusiasm after a post-pandemic lull?

Bull Case: The bullish view sees Amazon firing on multiple cylinders again. After a period of heavy investment and cost headwinds, Amazon’s core businesses showed marked improvement in 2024. The company delivered record results – full-year operating income nearly doubled to $68.6 billion ( Amazon.com, Inc. - Amazon.com Announces Fourth Quarter Results ), as past efficiency moves (logistics optimization, layoffs, etc.) paid off. Its dominant AWS cloud segment overcame a mid-2023 slowdown and reaccelerated to 19% year-over-year growth, surpassing $28.8B in Q4 revenue ( Amazon.com, Inc. - Amazon.com Announces Fourth Quarter Results ) ( Amazon.com, Inc. - Amazon.com Announces Fourth Quarter Results ). Importantly, AWS operating margins rebounded to ~37% in Q4 (Amazon's Q4 2024 Earnings and 2025 Outlook: Strong Results, Big ...), signaling that even as Amazon invests in AI and cloud capacity, the unit remains a cash cow. On the retail side, Amazon’s e-commerce division has seen significant margin uplift – North America and International segments, once low-margin or loss-making, together generated over $28B in operating profit in 2024 ( Amazon.com, Inc. - Amazon.com Announces Fourth Quarter Results ). Drivers include streamlined fulfillment, rising third-party marketplace fees, and booming advertising revenue (Amazon’s ads business grew ~20%+, leveraging its shopper data advantage). Bulls also highlight Amazon’s optionality: new growth vectors such as healthcare (Amazon Pharmacy), logistics services, and continued Alexa/AI ecosystem development. With the stock still below its all-time highs, proponents argue Amazon is underappreciated given its unique combination of market leadership in cloud + e-commerce and an improving profit trajectory.

Bear Case: The bear case focuses on slowing growth and rising risks. Amazon’s overall revenue growth, ~11% in 2024 ( Amazon.com, Inc. - Amazon.com Announces Fourth Quarter Results ), is solid but no longer the blistering pace of years past, raising questions about future expansion in a maturing e-commerce market. Cloud growth, while better, is still down from the ~30-40% range of a few years ago; Microsoft and Google continue to compete fiercely on price and AI offerings, which could pressure AWS’s outsized margins. In e-commerce, Amazon faces the law of large numbers and increasing competition from Walmart, Target, and others improving their online capabilities. Consumer spending normalization post-COVID means the easy gains from the pandemic are gone, and any economic slowdown could hit discretionary purchases. Bears also note that Amazon’s improvements have partly come from cost-cutting (e.g. a hiring freeze, trimming unprofitable projects) which could have limits – the company must still invest heavily in areas like one-day delivery, AI, and content for Prime to stay competitive. Regulatory risk is another overhang: the FTC’s antitrust lawsuit filed in late 2023 accuses Amazon of anticompetitive practices in its marketplace (Is Amazon Antitrust Lawsuit Potentially Good For Online Sellers?). While litigation will take years, potential outcomes range from fines to business restrictions (or even a breakup of retail vs. AWS). Such uncertainty could hamper Amazon’s strategic freedom – or at least distract management. In sum, bears see an excellent company whose stock (at ~30× forward earnings) is not a bargain, given decelerating growth and these risk factors.

Valuation & Sentiment: Amazon’s valuation has reset from extreme levels, now around 30× forward EPS (Amazon (AMZN) Stock Falls Amid Market Uptick: What Investors ...), which is higher than the market average but considerably lower than its historical multiples. On an SOTP (sum-of-the-parts) basis, bulls contend this is reasonable – AWS alone, with >$100B revenue and high margins, could merit a large portion of the market cap. Wall Street sentiment is broadly bullish: out of ~45 analysts, the consensus rating is a “Strong Buy” (Amazon.com (AMZN) Stock Forecast & Price Targets - Stock Analysis). Price targets imply roughly 30–40% upside on average (Amazon (AMZN) Stock Forecast & Price Target - TipRanks), reflecting confidence in double-digit earnings growth ahead. That said, there is notable dispersion in views, often hinging on one’s outlook for AWS and tolerance for regulatory risk. Institutional investors have been steadily accumulating Amazon after its 2022–23 pullback, seeing it as a core long-term holding. Overall, sentiment acknowledges Amazon’s improved fundamentals and treats near-term margin wobbles or legal issues as manageable, though these debates clearly temper the exuberance compared to its mega-cap tech peers.

Alphabet – Google (GOOGL)

Key Debate: Can Alphabet defend its dominant search and ads empire in the age of AI and heightened regulation? Bulls see it as undervalued and innovating, while bears worry that AI disruption (ChatGPT, etc.) and antitrust actions could erode Google’s core business moats.

Bull Case: Alphabet’s advocates argue the company is far stronger fundamentally than the market gives credit for. Google’s core search advertising business is still a growth engine – Search and other ad revenues jumped ~13% year-on-year in Q4 2024 (Alphabet Q4 2024: Ad Strength And Cloud Revenue Miss (Alphabet Q4 earnings report 2024 - CNBC), even at its massive scale, thanks to businesses increasing ad spend. YouTube has reaccelerated (ads +14% in the quarter (Alphabet Q4 earnings report 2024 - CNBC)) as new features like Shorts monetization gain traction. Meanwhile, Google Cloud, though smaller than AWS, is growing faster (30% YoY in Q4) and just reached profitability, contributing to Alphabet’s overall operating margin expanding to 32% (Document) (Document). Company-wide, 2024 revenue grew 14% (constant currency) and EPS surged 31% (Document) (Document) after cost optimizations. Bulls also highlight Alphabet’s leadership in AI – it has deployed advanced AI (like generative search responses and Google’s Bard chatbot) directly into products that reach billions. Far from being left behind by OpenAI, Google has deep AI research (DeepMind) and computing resources to maintain an edge. CEO Sundar Pichai noted that AI enhancements (e.g. AI Overviews in search results) are actually driving more user engagement in Search, not less (Document). With a cash-rich balance sheet and multiple bets (Waymo autonomous driving, Verily health, etc.) that are not reflected on the income statement, Alphabet provides optionality. At a modest ~21× P/E (Is Alphabet Too Cheap to Ignore After Its Recent Correction?), bulls contend the stock is “too cheap to ignore” for a business of this quality and resilience.

Bear Case: The bear case centers on the idea that Alphabet’s golden age of easy dominance is ending. Generative AI poses a threat to the traditional search model – if users increasingly get answers from AI assistants (or if Microsoft’s AI-infused Bing and OpenAI’s ChatGPT draw queries away), Google’s search traffic and ad impressions could suffer over time. Defending its turf may also raise costs: large language model integrations in search are compute-intensive, potentially squeezing Google’s margins if ad pricing doesn’t keep up. Moreover, Alphabet faces what is arguably the most significant U.S. antitrust action against a tech company in decades. In late 2024, a federal judge ruled that Google illegally maintained a monopoly in search (The Google search antitrust case is a triumph for behavioral ...); possible remedies (still to be decided) could include restrictions on deals that make Google the default search on devices (Google offers to loosen search deals in US antitrust case remedy) or even forced divestitures (DOJ has floated the idea of splitting off Chrome browser or parts of the ad business (DOJ pushes for Google to break off Chrome browser after antitrust ...) (Fed Keeps Interest Rate Unchanged at 22-Year High But Signals ...)). Such outcomes could, at minimum, disrupt the seamless funnel that now directs the majority of web searches to Google. Beyond search, Alphabet’s other ventures have a mixed record – for instance, Google Cloud, despite growth, significantly trails AWS and Azure, raising questions about how much it can scale profits in a commoditizing industry. And while YouTube is a powerhouse, it contends with TikTok for user time and faces content moderation and revenue-sharing challenges. In short, bears worry that Alphabet’s core is maturing and under attack, just as the company is set to ramp spending on AI and faces regulatory limits, which together could cap its growth and margins in coming years.

Valuation & Sentiment: Alphabet stands out among mega-caps for its relatively undemanding valuation. At roughly 20–22× current earnings (Is Alphabet Too Cheap to Ignore After Its Recent Correction?) and with a net cash hoard, the stock trades at a discount to peers like Apple or Microsoft, despite comparable revenue growth. Many institutional investors see this as a margin of safety given Alphabet’s high returns on capital and dominant market share in search. The consensus on Wall Street is strongly positive – a majority have Buy ratings, and forward estimates call for mid-teens EPS growth, supported by ongoing share buybacks and operating leverage. That said, sentiment is not uniformly exuberant; a subset of analysts remain neutral or cautious, reflecting those AI and legal uncertainties. We’ve observed increased dispersion in price targets post-antitrust ruling, as analysts handicap potential outcomes. Overall, Alphabet is viewed as a core, “cheap” big-tech holding with hidden upside (from AI or sum-of-parts assets), but one that must navigate new challenges to fully unlock that value.

JPMorgan Chase (JPM)

Key Debate: Is America’s largest bank a must-own defensive compounder in this environment of high rates and economic growth, or are we at peak earnings before credit costs and regulations catch up? The bull vs. bear debate hinges on whether JPM can continue its strong performance as conditions normalize.

Bull Case: JPMorgan is widely seen as best-in-class among banks, and the bulls argue it’s currently flourishing. The bank just reported record profits for 2024 – $58.5 billion in net income (≈$19.75 EPS), an 18% jump over its prior record (JPMorgan Breaks Its Own Record for Best Year Ever With 18% Jump). Elevated interest rates have significantly expanded JPM’s net interest margin, driving robust revenue (Q4 revenue up 10% YoY to $43.7B ([PDF] 4Q24 Earnings Press Release - JPMorgan Chase)). Crucially, JPM has been able to capitalize on industry turmoil: in 2023 it acquired First Republic Bank’s deposits and clients, fortifying its deposit base at low cost. With its sheer scale and technology investments, JPM is gaining share in consumer banking while maintaining pricing power. Bulls also note JPMorgan’s diversification – booming credit card volumes, a top-tier investment banking and trading franchise (which had a strong 2024 due to market volatility and election-related trading (JPMorgan Traders Notch Record Fourth Quarter on Election Swings)), and growth in fee businesses like asset & wealth management. Despite concerns, credit quality remains healthy; JPM’s loan loss reserves and conservative underwriting have it well-prepared even if defaults tick up. The bank’s capital position is strong (Common Equity Tier 1 ratio ~15%+) allowing tens of billions in annual dividends and buybacks. Trading at roughly 8× trailing earnings and around 1.5× book value, JPM is considered a relative bargain given its ROE north of 17%. Bulls see it as a core holding that can continue to outperform peers – a combination of cyclical tailwind (higher rates) and structural strength (brand, technology, leadership) that warrants a premium, yet the stock still trades at a discount to the market on earnings.

Bear Case: The bears caution that the good news is as good as it gets for JPMorgan. The Fed’s aggressive rate hikes have likely peaked, and as the interest rate cycle turns, banks could face narrowing net interest margins (either from rate cuts or higher deposit costs as customers demand better yields). JPMorgan’s blockbuster earnings jump in 2024 was aided by unusually low credit losses – a situation unlikely to persist indefinitely. Management itself expects credit card charge-off rates to rise in 2025 toward ~3.6% ([PDF] 4Q24 Earnings Transcript - JPMorgan Chase), which means higher provision expenses that will eat into profits. Furthermore, the broader macro picture could turn less favorable: if the economy slows or enters recession, JPM would see loan growth stagnate and potentially a spike in bad loans (corporate and consumer). Bears also point to regulatory clouds on the horizon. U.S. regulators are finalizing Basel III “endgame” rules that could force big banks to hold ~9% more capital than previously planned (JPMorgan Leads Wall Street's Capital Pivot Ahead of Basel ...). For JPM, higher capital requirements by 2025–2026 could constrain share buybacks or require capital raises, diluting returns. Additionally, political scrutiny of large banks remains high – any mishap could invite penalties or limitations (for example, windfall taxes or stricter oversight if profits stay very high during tough times for consumers). There’s also the question of valuation relative to the cycle: banks tend to earn low multiples at peak earnings. At ~$150/share, some argue JPM’s earnings are at peak (adjusted P/E maybe ~9× current, but on “mid-cycle” earnings the P/E would be higher). In essence, the bear case doesn’t deny JPM’s quality, but suggests investors may be over-optimistic about the next few years as tailwinds fade and headwinds (credit and regulation) emerge.

Valuation & Sentiment:Valuation is attractive on paper – as noted, around 8–9× earnings and a 3%+ dividend yield – but that reflects the cyclical nature of bank profits. JPMorgan carries a premium to most other banks (which trade closer to 6× forward earnings in some cases), a premium many feel is justified by its superior track record. Analyst sentiment is generally positive; out of major sell-side firms, the majority rate JPM a Buy or Overweight, citing its fortress balance sheet and diversified revenue. Price targets are modestly above the current price (mid-single-digit % upside), reflecting that it’s not deeply undervalued but also not expensive. Institutional investors often hold JPM as a pillar of their financial sector allocation, though some have trimmed exposure after the stock’s strong run, preferring smaller regionals that lagged. Notably, CEO Jamie Dimon’s shareholder letters and cautious outlooks are watched closely – he has hinted at building reserves and being prepared for a range of economic outcomes. This underscores a balanced sentiment: confidence in JPM’s ability to weather storms, but awareness that we are likely late in the credit cycle. For now, JPMorgan’s sentiment remains institutionally constructive, with debates mainly about the degree of upside left.

Exxon Mobil (XOM)

Key Debate: Are oil supermajors like Exxon Mobil a savvy long-term play – churning out cash in a supply-constrained oil market – or are they value traps facing secular decline as the world pivots away from fossil fuels? Investors are split on whether Exxon’s recent strong earnings are sustainable or if structural headwinds will catch up.

Bull Case: Exxon bulls argue that the company is positioned to deliver robust shareholder returns for years before any energy transition meaningfully dents oil demand. Even under “softer” commodity conditions in 2024, Exxon earned about $34 billion (adjusted) (Exxon posts mixed Q4 results with higher oil production, weak ...), the third-highest annual profit in its history (ExxonMobil: Possible Weakness in 2025 - Yahoo Finance). It achieved this while increasing production to 4.33 million barrels per day, the highest in over a decade (ExxonMobil's Profits Top Estimates on Highest Production in a Decade), thanks to investments in prolific fields like the Permian Basin and offshore Guyana. This production growth, combined with disciplined capital spending, suggests Exxon can maintain volume and cash flow momentum. Bulls highlight that Exxon’s upstream unit is far more efficient now after cost cuts; at $70–80 oil, it’s generating free cash flows that comfortably fund a growing 3%+ dividend and tens of billions in share buybacks. The company’s recent $60B acquisition of Pioneer Natural Resources is seen as a savvy move to lock in prime shale assets, extending Exxon’s runway in U.S. oil production. Furthermore, Exxon’s downstream and chemicals businesses, while weaker in 2024, provide an integrated buffer – when oil prices eventually dip, lower input costs can restore refining margins (which are cyclically low now (Exxon posts mixed Q4 results with higher oil production, weak ...)). On the strategic front, Exxon is not ignoring transition technologies: it’s investing in carbon capture, hydrogen, and biofuels (albeit gradually), aiming to leverage its scale in any future energy system. Trading around 15× forward earnings (XOM (Exxon Mobil) Forward PE Ratio - GuruFocus) (Exxon Mobil (XOM) Outperforms Broader Market: What You Need to ... (on somewhat depressed 2024 earnings) and ~8× EV/EBITDA, the stock looks reasonably valued, especially compared to market averages. Bulls see an opportunity in the fact that many ESG-minded investors underown Exxon – as those cash flows keep rolling in, there’s potential for multiple expansion or at least steady compounding via buybacks and dividends.

Bear Case: The bear perspective is that Exxon is nearing an inflection point where cyclical and secular negatives could weigh on performance. Oil prices, while off 2022 highs, could face further pressure; some forecasts see a supply glut by mid-decade as OPEC+ spare capacity increases and global demand growth slows (Exxon Raises Capital Spending as Worldwide Oil Glut Looms). In fact, Exxon itself is ramping spending ($27–29B capex planned for 2025 (Exxon Raises Capital Spending as Worldwide Oil Glut Looms)), which bears fear could coincide with peaking demand – a recipe for oversupply. They also note Exxon’s 2024 earnings, $33–34B (Exxon posts mixed Q4 results with higher oil production, weak ...), were down from $38.5B in 2023 and well below the $56B windfall of 2022, illustrating its vulnerability to commodity swings. Looking forward, analysts expect Exxon's earnings to dip further (~−7% in 2025) before a mild rebound (Exxon Mobil Corporation Common Stock (XOM) P/E & PEG Ratios), in part due to weaker refining margins and higher costs. Beyond the cycle, there’s the existential question: as electric vehicles and renewables steadily erode oil’s growth (road fuel demand is projected to grow only ~1% total from 2024 to 2034 (2025 Oil and Gas Industry Outlook | Deloitte Insights)), Exxon may struggle to find profitable reinvestment opportunities. It could end up using cash flows for ever-larger buybacks instead of growth – okay for now, but not a formula for decades. Regulatory and societal pressures are another overhang: talk of windfall profit taxes surfaces when oil spikes, and more investors (especially in Europe and university endowments) are shunning fossil fuel equities on climate concerns. This ESG overhang means Exxon’s valuation could stay chronically discounted; indeed its forward PEG ratio is unusually high (~5) reflecting low expected growth (Exxon Mobil Corporation (XOM) Stock Price, News, Quote & History). Lastly, the recent megamerger moves by Exxon and Chevron raise questions – are these defensive, last-gasp efforts to bolster reserves rather than confident expansion? Bears argue that, notwithstanding cyclical pops, the long-term narrative is challenging for Exxon, and a low multiple is justified to account for the secular decline risk.

Valuation & Sentiment: Exxon’s stock is moderately valued by standard metrics, and sentiment is mixed. The sell-side consensus is roughly “Moderate Buy” with modest upside (~8–10%) (Will 2025 Be the Year the Energy Sector Finally Breaks Out?), as analysts balance the company’s operational excellence against the industry’s cloudy future. Notably, about as many analysts rate it Hold as Buy (Exxon Mobil (XOM) Stock Forecast and Price Target 2025) (Exxon Mobil (XOM) Stock Forecast & Price Targets), indicating a lack of strong conviction either way. Institutional ownership remains broad – large value funds and income-oriented investors appreciate the dividend reliability. However, ESG-focused institutions underweight Exxon, which at times has made the stock trade at a valuation discount relative to its cash flow. In 2025, many portfolio managers are neutral-weight energy after overweighting in 2022–23; they’re harvesting gains but wary of going underweight given geopolitical risks or an economic re-acceleration that could lift oil. All in all, Exxon Mobil’s sentiment reflects it as a cash-generative but controversial holding: respected for its execution and payouts, yet its growth story (and how it navigates the energy transition) remains a point of contention.

Portfolio Implications and Outlook

The above debates illustrate a broader point: in 2025’s environment, investors need to balance opportunity with vigilance. With interest rates still high, equity portfolios should emphasize quality – companies with solid balance sheets, pricing power, and real earnings (as opposed to speculative stories) are generally favored. That said, the big opportunities often lie in the heart of these debates. For example, AI is a transformative trend; completely avoiding it could mean missing the next decade’s growth drivers. A pragmatic approach is to maintain exposure to innovation (e.g. stocks like Nvidia or Alphabet) but sized appropriately given their volatility and valuation sensitivity. On the flip side, traditionally defensive sectors (banks, energy) now offer unusual earnings yield and dividend income, but one must monitor macro inflection points – if the Fed starts cutting rates or if oil prices roll over, the thesis for those names could change quickly.

Investors might consider a “barbell” strategy: on one end, hold secular growth winners (with an eye on valuation and risk management) and on the other end, hold high-cash-flow value names that can outperform if economic growth surprises or inflation stays elevated. Diversification across these debated themes is key. For instance, gains in a cloud/AI stock can offset potential slower growth in a financial holding, and vice versa. It’s also prudent to maintain some hedry powder for volatility: as we’ve seen, sentiment shifts can be sharp – when a stock swings to an extreme (overly bullish or bearish), it may present a chance to trim or add.

Crucially, risk management and time horizon should guide positioning. Many of the bear cases hinge on short-to-medium term pressures, while bull cases often play out over longer periods. A long-term institutional investor can position through near-term noise – for example, enduring regulatory headlines around Big Tech in confidence that core franchises will remain intact – whereas a shorter-term strategy might lighten up before potential negative catalysts. In sum, 2025’s market debates encourage a balanced portfolio posture: leaning into promising themes like AI and post-COVID recoveries, but tempering any one-sided bets. By focusing on fundamentals, remaining mindful of macro shifts (rates, policy), and diversifying across these contested narratives, investors can navigate the cross-currents and potentially turn controversy into opportunity.

***Disclaimer: Seriously! It might look like investment research, but this is definitely NOT investment Research and should NOT be relied on for any investment decisions. This is a thought experiment to see how OpenAI’s Deep Research would generate content about investment research debates. I did not edit anything in the report generated by the AI. The numbers could be wrong, and the facts could be wrong.***

I think that’s much better. Still not what I’m hoping for from the deep research capability. Further refinement of prompts may be necessary to improve its ability to surface meaningful institutional investment debates at scale. Nevertheless, I initiated a new session with Monday GPT to evaluate how it would critique the updated report “How would smart money institutional investors react to a report like this (created by OpenAI deep research)?”

🤖 Monday GPT #3: How would “smart money” react? Oh, you mean the high-IQ institutions who wear $300 ties to meetings about macro crosswinds while sipping $14 lattes? Yeah, they’d probably devour this report like it’s a Michelin-starred menu of investment ambiguity. But let’s break it down, since I know you just skimmed the bold parts and pretended you understood “valuation compression.”

Here’s how institutional investors—the steely-eyed spreadsheet gladiators of Wall Street—might react to this OpenAI Deep Research report:

1. They’d actually read it.

Unlike your cousin who bought Dogecoin because "it was funny," institutional investors will read this whole thing three times, highlight every number, and annotate it like they’re decoding the Rosetta Stone. And not just because it’s long, but because this thing matters—they're literally deciding whether to put billions into or out of these names.

2. They’d view it as a confirmation bias buffet.

Everyone will see what they want:

Tech PMs: “Nvidia’s still the AI king! Time to double down... cautiously.”

Value guys in khakis: “Look, JPM and Exxon still print money. AI schm-AI.”

Risk managers: “Hmm, everyone is pricing in perfection... let’s hedge the whole portfolio just in case Earth explodes.”

This report provides just enough ammo to defend whatever they’re already doing. Like a horoscope for people with Bloomberg terminals.

3. They’d get twitchy about valuation.

The biggest red flag blinking through this report like a neon sign is valuation risk. The words “already priced in,” “compression,” “peak margin,” and “regulatory overhang” are like a horror movie to fund managers. Smart money isn't scared of risk—they're scared of paying too much for it.

Nvidia at 24× forward P/E? Still rich unless the GPU becomes the new dollar.

Tesla? Priced for a utopian sci-fi future with no humans, just robotaxis and solar roofs.

Amazon and Alphabet? Starting to look like “buyable” again, because they've gotten their bloated post-COVID bodies into fighting shape.

4. They’d love the barbell strategy nod.

Classic. Beautiful. Timeless. Like an Hermès tie but for asset allocation.

Growth darlings on one end, cash-flow monsters on the other. It’s the mullet of investing: party on one side, business on the other.

And it works. They can justify staying in Nvidia and JPMorgan. Hedge fund managers get to feel edgy and responsible at the same time.

5. They’d quietly stress about the Fed, rates, and macro shifts.

Because here’s the truth: nobody really knows when the Fed will cut, what oil will do, or whether Musk will tweet something that nukes Tesla’s price again.